June 25, 2016 Update

Coming soon to a Walmart in your area …

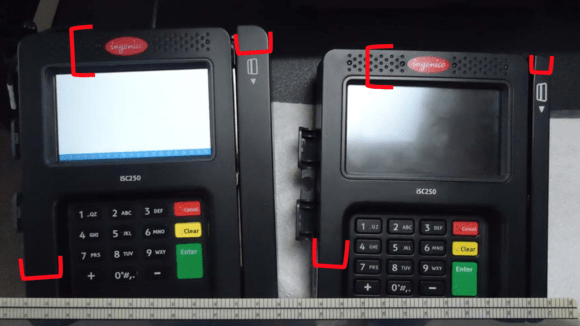

There’s a whole new generation of credit card skimmers at Walmart et al that are surprisingly good…

Can you spot the fake… from the real one?

….

Because the thieves have to snap the skimmer mask over-top the real credit card reader, the fake ~skimmer~ is a little wider, and a little taller.

Thanks to Krebs on Security for their ongoing excellent work…

http://krebsonsecurity.com/2016/06/how-to-spot-ingenico-self-checkout-skimmers/

************************

Jump to the bottom of this article for images of other card skimmers seen in the past in Yucatan (see bottom of article).

************************

Confused about the ins-and-outs of changing money in Mexico and the USA, how to get reliable exchange rates, plus some of the nitty gritty details on how the credit card, bank debit cards, currency exchange and ATM systems work? Rather than a dry discourse of skads of financial details and jargon that make our eyes glaze over, we’re going to try give you some tricks to make managing your travel dollars easily and well.

Some expat “experts” proclaim:

~~ Using a credit card will always give you the worst exchange rates anywhere in the world. ~~

~~ Credit cards always give the best exchange rates. ~~

~~ ATMs are the only way to go! ~~

~~ Try to get the official exchange rates! ~~

~~ None of us have enough money to ever get the published rate. ~~

~~ I have always used Traveler’s Checks. Aren’t they still the best choice? ~~

For the rest of us it basically, it all boils down to:

~~ Where can I change money? & How can I do it easily & well? ~~

At face glance, the first statements seem to conflict with each other, but knowledge of the vagaries of banks, credit cards, and currency markets might unravel these knots.

Let’s start with the low-hanging fruit, and then move on to the easy meat:

The exchange rates printed in newspapers and posted on good sites like “xe.com” are the floating rates on actual buy/sell transactions through that firm’s trading desks (like a stock market brokerage) that are reported as the midpoint of that particular currency market’s purchases and sales of a currency. Midmarket rates: the average of the latest buy and sell prices that are being paid in the currency markets for large transactions by banks and trading houses => neither the buy nor sale price and different rates for small tourist transactions vs. large transactions of millions of $$. The buying and selling prices of a currency are not the same, because the bank or currency exchange needs to be paid for providing the exchange service. e.g. Do we expect McDonalds to sell us a hot hamburger for at their cost of raw meat, a little ketchup, & a bun?

The next reality is that small $$ transactions cost the banks and exchange markets roughly the same to process as larger $$ transactions, (except for issues surrounding the float), so, the exchange rate you get depends on how much money you exchange per transaction. Here’s a simplified example of how this works for expats and travelers:

If a bank needs $2 of effort/overhead to process a transaction, then when Joe changes $100 at a bank and Sue changes $1,000 at the same bank at the same time, Sue should get a better exchange rate, because the bank’s $2 exchange cost/fee is 2% of Joe’s your $100 and the bank’s $2 exchange cost is just 0.2% of Sue’s transaction.

Savvy consumers may realize that there appears to be a gap between the reality of posted exchange rates at banks and currency exchanges, while Yucalandia just claimed that exchange rates are different for large v. small transactions. ~ What’s up with that? ~

The key is moxy. If you want special deals in life, you usually have to ask for them.

The best things in life are rarely blazoned on banners or trumpeted in ads.

Another Useful Reality:

Posted exchange rates at bank windows are not written in stone.

If you have a larger sum to change, ask to talk with a manager. We’ve gotten at least 1% and sometimes 1.5% better rates on every large exchange, but ya gotta ask !

Next, expect to wait an extra ½ hour as the manager pulls up his current mid-market rates, gets approval for the special rate, and then works with the teller to do a special transaction. If an extra ½ hour is worth $50 – $100 USD or more to you, then maybe it’s worth the wait?

Continuing:

Careful consumers who want the best overall exchange rates & lowest fees will:

1. Pick credit card companies that do not charge set fees or a % on your foreign transactions;

2. Use their credit card to make all possible international purchases to get the best rates;

3. Check with the merchant to see if they add fees/charges for using your for using a foreign credit card, especially on large purchases;

4. Make large charges only on days or periods when the exchange rates are to your liking.

5. Ask to talk with the bank manager or currency exchange manager to request a better (the best) rate when making large exchanges: We typically shave 1% and sometimes 1.5% off the best advertised rates.

6. Carry at least 2 credit cards from different agencies, in case one gets put on-hold. (See below for more on keeping your cards from being put on hold.)

7. Consider life outside the box: You can actually get the mid-market rate or better if you are clever & observant and can speak a little persuasion (Spanish or English). Try to spot a someone in the line at the bank who wants to exchange $$. If you see that the person has enough cash in hand to cover your exchange amount, and if they are exchanging their money for your currency, then you can politely offer to exchange with them at the mid-market rate, cutting the middleman out of the transaction. I have done this several times, and both buyer and seller walk away happy.

If you live in Mexico and get paid in pesos, you might also find you have friends who will gladly do wire transfers into your US account, so they can get pesos from you at the best rates. (We need US dollars and I sell pesos, so the expat gets the pesos they want and I get the dollars => win-win.)

Since large credit card companies, like VISA, process/exchange $10’s of millions of dollars per day, they get the best exchange rates, because they are the biggest customers in the daily exchange markets. VISA typically gives their CC customers using the card internationally the rate from close of the business day, along with their vig. Regardless of some common internet claims and advice to not use credit cards, by using a fee-free credit card, you generally get to piggy-back on the best exchange rates of the biggest players. You will never get the day’s best mid-market rate this way, (particularly if the intra-day market rates are fluctuating wildly due to uncertain economic times), but you can come very close with this approach.

This last “rule” can have some exceptions: Many merchants (in the US and around the world) hold their customer’s credit card transaction “receipts” for 1 business day to 3 business days before entering/processing/submitting/posting them to the credit card company. e.g. This delay can actually cause your Friday’s credit card purchase to be posted to the exchange markets as late as the following Wednesday…

This means that you can sometimes come out a big winner or a big loser (by a few %) when using your credit card vs. an ATM card or Debit Card, because ATM companies & banks almost all post their transactions by 12:00 PM of that same day (Friday in our example). By using a Credit Card, if the mid-market currency rates change in your CC’s favor between Friday and Wednesday, you then get a better rate on Wednesday than the Friday posted exchange rate that you get from a Debit or ATM card. If the currency rates change in your favor between Friday and Wednesday =>

Woooo Hoooo !!!

If the currency rates change against you on your CC purchase vs. ATM between Friday and Wednesday

=> Waaaaaaaah !!

To fill out the picture: Debit card transactions from many banks are be posted to your checking account almost immediately, which means you get the exchange rate of that moment, which may be different than the “official” posted rate for the day, because the “official posted rates” are actually just the trading-day’s ending rate: the price of last transactions of the exchange market’s day. ~ Just like stock prices: Intra-day rates can swing wildly sometimes during a day, but the newspapers and historical charts & tables only show the ONE rate for that LAST individual transaction just before the bell rings. **(This means the rate you got might not be close to the historical posted exchange rate for that day due to market vagaries.)

So, if you rely on individual expat stories on internet forums to form your opinions, you’ll usually get a scatter-gun blast of opinions: some diss-ing credit card use and swearing-by some currency exchange or ATM, while others swear-at their currency exchange or ATM (particularly if they get nicked for ATM fees, bank fees, and international usage fees).

Hope this helps explain some of the apparent contradictions and irregularities in CC, Debit Card, and Exchange Rate issues.

Other Tips for Successfully Using your ATM, Debit, or Credit Cards while Traveling:

When traveling, it can be a good good practice to notify your Credit Card company or Bank Card issuer that you are planning to travel beyond your usual haunts. Still, when talking on the phone with your Credit Card company phone operator, there are often some extra hidden hoops that their typical phone representatives aren’t aware of.

Credit card company’s Consumer Fraud departments and Security Departments operate in ways that the typical CC company phone rep doesn’t know about. Many card companies have computer programs that automatically limit the number of withdrawals or transactions that are allowed outside of the user’s home area. Some have daily $$ limits that trigger automatic holds on accounts. Some of these rules are only triggered once every 24 hours (when their computers connect with the main ATM computers and CC clearing house companies in the middle of the night – updating data once daily at midnight). This means that your card may work for a day when overseas – or even for a few days (over the weekend), but then “boom” the merchants post your debits/purchases a day or so later, triggering the CC companies’ anti-fraud systems.

You can often remedy these problems by calling your bank’s or CC company’s normal phone number, but instead, specifically ask to speak to their Security Department reps. When connected to the Security Dept rep, then ask them to:

“Please put a note in my account’s Comments File saying that I will be traveling in the following countries: ______, leaving the US on this date: ________, and returning on this date: ________. I expect to visit the following cities during this time period: _________. Please keep my debit/credit card access open and approve any charges for my travels for this period (dates): __________”

Some credit card company’s fraud detection software will even flag travel to a different state and put a hold on your card due to “unusual activity”. e.g. Colorado residents find that traveling to the exotic and far-off hinterlands of Nebraska will often trigger the rejection of successive gasoline purchase attempts, so, some savvy travelers even log their inside-the-country travel plans with the CC companies before leaving home.

I also like to ask the Security Dept rep exactly how their system works, and how I might improve my chances of using their card successfully during my travels…. (Maybe their systems and policies change over time???) Usually the rep can tell you how to best keep your cards working and make the cash flow smoothly.

If there is a suspected problem with a card, a human in the Security Department is supposed to look at (review) the customer’s Comments Files after the computer automatically triggers the first stops/suspensions on unusual transactions. This means that you may have a few transactions denied (typically cards are suspended for one day) when first using the card in a new country. Later in the day, when a human looks at your account to evaluate the potentially fraudulent activities, the human sees your Comments File notes, and then re-approves your card for further use. Even if you follow this advice, the company’s computers still can flag your account for suspicious activity, and you may need to call your company to get the “hold” released. It can be a life saver if you keep the CC company’s international phone numbers and also carry a second credit card when traveling.

If there is a suspected problem with a card, a human in the Security Department is supposed to look at (review) the customer’s Comments Files after the computer automatically triggers the first stops/suspensions on unusual transactions. This means that you may have a few transactions denied (typically cards are suspended for one day) when first using the card in a new country. Later in the day, when a human looks at your account to evaluate the potentially fraudulent activities, the human sees your Comments File notes, and then re-approves your card for further use. Even if you follow this advice, the company’s computers still can flag your account for suspicious activity, and you may need to call your company to get the “hold” released. It can be a life saver if you keep the CC company’s international phone numbers and also carry a second credit card when traveling.

Sometimes the timing of these stops, holds, or daily limits seems strange, because the merchants and banks may only post your charges/withdrawals at the end of the day or even up to 5 business days later. This means you can’t trust the “current account balance” printed out by most ATMs. Even if you use some cute app to check your account’s posted activites and balances and limits online, you can get a false sense of security from apparently having lots of cash left, since these on-line statements only reflect the previous days merchant postings: Their figures are not actually “current”.

The Pitfalls of Using ATMs or Cash Advances on Credit Cards at ATMs:

First, be aware that just like Canada and the USA, identity theft can take the simple form of a thief discreetly stealing your ATM card’s information and using it to make false charges. The thieves have gone high-tech, no longer lurking around ATMs to try to clip our information. Instead they are installing very-professional official-looking injection-molded plastic covers just over the ATM’s card slot. Their plastic cover includes some compact microelectronics that capture your card’s personal information, replicate it, sell it, and then they begin making lots of charges in far-off States, within hours of “cloning” your card,

VERSUS

and

Look official, don’t they?

You might notice how many of their skimmer/mask/cloner blocks the normal LEDs, so you can’t see the little lights. This is one tip that the ATM may not be safe to use (as my Yucateco brother-in-law did not notice). But the last foto is particularly troubling, because the skimmer/cloner has a clear shield that allows the LEDs to shine through the mask. For this reason, many Mexican banks have modified their card entry slots to have a bank of 6-8 large and bright LEDs. Look for that bank of un-covered LEDs….

Note how this professionally made skimmer has no LEDs showing.

And, yes, our local Yucateco Banamex ATMs had a big problem with this last August. My wife’s brother had our card cloned in Progreso. We were quickly hit with multiple $4,000 – $6,000 charges made in Vera Cruz and Guadalajara. Banamex did not reimburse the money until 3 months later, even though over 400 people’s cards were cloned.

Another person in my wife’s workplace noticed that the slot to his favorite ATM was loose, so, he shook it – and it moved – but he used it anyway and he too is working with Banamex to get his money back.

Check that slot on the ATM, before you slide your card in, and use one hand to block any cameras views of your other hand when typing in your PIN / NIP.

When planning your trips finances, remember that many many smaller Mexican towns of 5,000 people or less have neither ATMs nor banks, so, it’s generally best to make your exchanges in larger cities, like Progreso or Merida before making forays out into the bush.

There is one last item with ATM usage that occasionally bites less-experienced foreign travelers: taking cash advances on their credit cards. It all seems so simple: walk up to the ATM, pop in your credit card, enter your NIP (Spanish for PIN), decipher the menus, push a few buttons, and then enjoy the sweet zhhhht-zu-zeet-pwwwwht whirring sounds that means the machine will soon spit out a neat stack of crisp bills. Like a slot machine that always pays-off, right? Sweeeet…?

Ba-dum…. BA-dum… BA-dum, BAA-dum…… Is anyone else hearing the theme from Jaws?

Be afraid, be very afraid: You have just stepped into “their“ world, and “they” now own a little piece of you.

Why? Cash advances are treated very differently than all other credit card transactions: a world where grace periods and on-time payments do not apply: A world where the normal rules of interest and finance fees no longer apply.

In the fine print of your credit card company’s agreement, you give them the right to charge interest and often daily fees on cash advances from the moment you receive your neat stack of crisp new bills. This means that interest and fees accrue every day until you pay the entire credit card balance off in full. If you use the card for any credit purchases after you make a cash advance, the CC company then applies your new payments only to the latest CC purchase(s) and not the cash advance.

If you continue to make any CC purchases that are larger than the old cash advance, they never have to apply any of your payments to the old cash advance, because once you take a cash advance, the grace period terms no longer apply, and you then owe interest and fees on all subsequent transactions. The CC company can then endlessly charge interest and monthly finance charges & fees, until you pay off all balances and all accrued interest and fees in full.

There are 2 ways to get out of this loop. If you are a check-user: Estimate how long it will take the mail to deliver your payment-by-check to the CC company, and add a few days to that date. Call the credit card company and ask their phone rep what the precise total of balances, charges, interest, and all fees will be on your account as of that projected mail delivery date. Next, make your check out for slighty more ($10?) than their estimated amount, in case the phone rep made a mistake. Send your check out that day, and DO NOT USE THE CARD OR OTHER CARDS ON THAT ACCOUNT FOR ANY PURCHASES UNTIL YOUR PAYMENT IS RECEIVED and RECORDED by the CC company, showing an official ZERO BALANCE.

A second approach is to call the credit card company, and have them tell you the exact total of your balance(s), including that day’s interest and any and all fees owed up to that moment. Next, have your checking account in hand and ask the phone rep to accept a direct transfer from your bank account to them.

If it is after 1:00 PM, the request may not process that day, so, you might have to authorize a slightly larger transfer to pay for another day’s interest and fees. Give the CC phone rep your bank routing number and your account number. Ask the rep when your transfer will be posted, and get the rep to tell you that “yes, your current balance is zero” and “there are no more fees, charges, or interest owed”.

This method of transferring cash directly avoids mail issues, but some banks and some CC companies charge $5 – $10 for using this method.

Using Airport Currency Exchanges, Casas de Cambios or Banks to Change Money:

When you change from dollars/loonies/pounds to pesos, realize that most airport cambio/exchange offices give some of the worst rates. Small store-front or kiosk casas de cambio also tend to give horrible rates, often charging 15% fees for making the exchanges.** This means that bank ATMs are often your best bet, but using the bank teller may be just as good, or maybe better. Note that the bank rates posted in the bank windows (in Mexico) do not actually apply – they are just past numbers that are not frequently updated, which means that they are not current.

**Exception to excessively high charges by Airport Currency Exchanges: In the main terminal of Benito Juarez airport, between the big waiting area of Gate19 and the International Gates area, there is… a long hallway. About halfway down that hallway, there are one or two Currency Exchange windows that offer the best rates we have ever seen for people selling pesos and wanting US dollars. The teller at one window explained that their main business generated a lot of bills in Pesos, and that their income is in Dollars, so, they give GREAT exchange rates – even though they are in an airport.

Quirks of Banking in Yucatan: The rate you get from the bank or ATM are based on the exchange rate for that short period (½ hour?). If you are changing $$ or Pounds for Pesos, then just about any bank works – as long as you have your passport. If you want to change your Pesos back into USD or Pounds, you probably have to do that in Progreso:

Most Merida banks do not keep foreign currency in their branches – they generally buy foreign currency, but they typically do not sell foreign currency, because Merida has so little tourism from foreigners – though it’s a big destination for Mexican tourists. Since the Progreso banks get lots of foreign currency – especially US dollars – they have USD to sell, and give pretty good rates. Still, not even all banks buy all currencies. Some Mexican branch banks are refusing to accept Loonies or Pounds or Euros, accepting only US dollars. They just don’t do enough trading in these currencies to make it worth it to accept them.

Travelers Checks:

Travelers Checks were once the gold-standard of safe secure money for international travelers. This is no longer true. In many countries, Travelers checks are now the pariah of international travelers, because so few merchants and so few banks accept them. Some tourists spend precious travel hours trying to find a place to cash them, even in big cities like Merida. To our knowledge, there is one place in Merida (in Hotel Fiesta Americana) that cashes them.

Instead, bring your bank card along to make ATM withdrawals, and bring 2 credit cards, preferably Master Card or VISA, along in case one gets a hold put on it. No, we don’t own stock in VISA, but we advise using them because fewer Mexican merchants accept American Express or Discover, but that is changing…

Hope all these financial details haven’t overwhelmed or dulled your senses too badly.

Disclaimer: This information is not meant as legal advice. It is for educational and informational purposes only. Government and banking policies vary between offices and companies, so your personal experiences may vary.

* * * *

Feel free to copy while giving proper attribution: YucaLandia/Surviving Yucatan.

© Steven M. Fry

Read-on MacDuff . . .

Pingback: Banking, Exchanging Currency, & Using Credit Cards & ATMs in Mexico | Surviving Yucatan

Great insight Steve!

Hmm… The photo that appears just about the end of your article… is that you? Looks like researching this comprehensive review took a lot out of you! Having noticed that you are an old fashion type of guy, at least in the sense that you prefer to pay in cash, all the more remarkable how well informed you are with those nastily convenient stiff plastic cards.

A bit more on credit cards (and debit cards): your bank may expect you to respond rapidly (as within hours or a day) to security holds they place on their computers’ noting “unusual” behavior. Depending on the institution, and perhaps your account settings, that could be an email, SMS message, or (unlikely if you are traveling out of country) a phone call.

Not responding can result in further attempts to use the card being denied, even though you have informed the institution of your travel plans.. One credit card I have, CapitalOne, has on multiple occasions taken a “note” on my account to expect and allow a monthly charge for Cablemas, yet from time to time I have to go through their security verification song and dance.

(I twice went to Cablemas to change the billing to a different card, but that has not happened.)

One further comment. When paying, as in a restaurant, typically the seller or waiter will disappear with your card. Many times I follow the waiter and carefully watch the billing process. My only error is not being sure to do that all the time.

ReadingTerminal,

Excellent advice and good observations.

steve

Pingback: How to Move Money from the USA to Mexico: Checks, Wire Transfers, ATMs | Surviving Yucatan

Great and comprehensive article Steve…

And after “reading terminal”‘s comment I will review and update my bank/CC/ATM company’s contact info to include my MagicJack phone number as a first contact option along with my e-mail etc.

Pingback: Watch for New Generation Credit Card Skimmers … Walmart | Surviving Yucatan

Pingback: ATM Fraud & Credit Card Skimmers: New App Detects Thieve’s Hardware on ATMs & Card Scanners | Surviving Yucatan

How much do the exchange rates vary from bank to bank? Is there a particular bank that generally has the highest rate?

Hi Brian,

It all depends on whether you’re using credit cards (which give you the very-best exchange rates) when making a purchase.

e.g. If you want to buy a car, you generally get the best exchange rate by buying the car with a US~Canadian credit card like Mastercard or Visa – meaning you get that day’s mid-market rate that Visa gets on their $10’s of millions of $$/pesos exchanged.

Local banks in the USA & Canada tend to give very crummy rates.

If you choose to bring down US cash, you have to check with each local banks to see if they will change it. Most banks require you to have an account. Casas de cambio take an extra 3% – 5% vs bank transfers. … The local bank branches have one published rate that they give to small transactions, but if you ask to talk with an account manager about changing a bigger sum (say $3,000 to $15,000 US dollars), the account manager calls the bank’s main exchange office (in far off Monterrey etc), and the bank’s main office issues a special rate that’s good for ½ hour to an hour.

There are times (days-weeks) when Mexican banks think the MXN peso is going to get weaker, so the Mexican banks will pay a premium rate to buy US dollars (much better than published exchange rates). … Other times, the SAME Mexican banks thing the MXN peso is going to get stronger, and they do NOT want US dollars, so they pay shitty rates for a few days or a few weeks.

Does that make sense? … We place an order for an exchange with our Scotiabank rep, and she calls us when their Scotiabank rate hits that value, and she locks in our exchange at that target rate we told her. We then have to go into Scotiabank within 30 minutes or an hour to sign-off & approve the transfer~exchange.

??

steve

Please do not post my previous comment, due to personal content.

Thanks!

Hi Brian,

Understood.

As an admin, I have the authority to edit people’s posts … so I edited-out the personal info.

Happy Trails,

steve

Pingback: Using Banks, Credit Cards & ATMs in Mexico -

Pingback: Using Banks, Credit Cards & ATMs in Mexico | The Yucatan Post